Compound interest refers to the interest applied to a loan or deposit amount. It is one of the most commonly used financial concepts in our daily lives. Compound interest means that both the principal amount and the interest earned during each period are added together. In contrast to simple interest, compound interest can significantly boost your returns over time.

If you have a deposit account and compound interest is applied, you would typically notice that your account receives a certain amount of interest annually when you observe your bank transactions. When you look at the annual yield of your deposit account, you will observe that the interest increases sequentially. In this article, we will take a look at what compound interest is and how it is calculated.

What is Compound Interest?

Before diving into the details and formulas, let's take a brief look at what compound interest actually means.

When your deposit returns are calculated using compound interest, you don't just earn interest on the principal amount, but you also earn interest on the interest you earned over time. Compound interest is a process where you add the interest earned on your principal amount back to the principal, which results in earning even more interest.

To give a short example, let's say you have a savings account with 1,000 TL, and this account earns 5% interest annually. In the first year, you will earn 50 TL, and your account balance will become 1,050 TL. In the second year, you will earn 5% interest on 1,050 TL, which amounts to 52.50 TL, and your account balance will become 1,102.50 TL by the end of the second year. This way, compared to other interest types, your balance will grow rapidly. Let's assume your deposit account goes through 30 years and you consistently earn a 5% annual interest rate throughout the whole period. At the end of 30 years, you will have a balance of 4,321.94 TL. Compound interest is added to your account at different time intervals, such as yearly, monthly, daily, or even continuously. The more frequently interest is compounded, the faster your principal amount will grow.

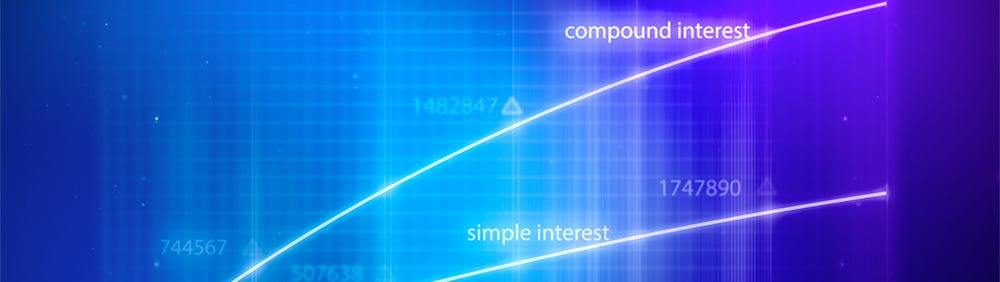

Difference Between Simple Interest and Compound Interest

Simple interest and compound interest work differently from each other. Simple interest is calculated based only on the principal amount and does not include the earned interest added back to the principal, as it is the case with compound interest.

To provide an example using simple interest, let's consider you have a deposit account with 1,000 TL, and you earn a 5% interest yield annually. In one year, you will only gain a profit of 50 TL. The interest earned is not added back to the principal. If you don't touch the money in your account for another year, you will again earn 50 TL in one year. Simple interest is generally used to calculate the interest on car loans and other short-term consumer loans.

Details of Compound Interest

When calculating compound interest, several factors need to be taken into consideration. Some of these factors directly affect your returns. When evaluating the compound interest process, it is essential to consider these factors.

Interest Rate: The interest rate paid or charged during the loan or deposit process. The higher the interest rate, the more money you earn or borrow.

Principal Amount: The amount of credit you took or the initial deposit amount in your account.

Compounding Frequency: One of the most critical factors for compound interest is the compounding frequency. It directly affects the growth rate of your balance. Compounding frequency can be daily, monthly, or yearly, for example.

Time Factor: How long you keep your money in a deposit account or how long you will take to repay your loan. This duration plays a crucial role in calculating your returns.

Compound Interest Formula

To calculate compound interest, there are a few methods, but don't worry, there are calculators available that can do the calculation for you. However, it's beneficial to understand the process.

The compound interest formula is as follows:

A = P (1 + [r / n]) ^ nt

A = The total amount of money after n years, including interest P = The principal amount (the initial deposit or the starting loan balance) r = Annual interest rate n = Number of times the interest is compounded per year t = Number of years the money is invested or borrowed

Also, the annual interest rate is divided by the compounding frequency to obtain the average interest rate per day, month, or year, depending on the compounding frequency.

Let's provide an example using the formula. Let's assume you have a deposit account with a 5% interest rate and an initial amount of 5,000 USD. Let's say the account compounds monthly for ten years. In this case, P (5,000 USD), r (0.05), n (12), and t (10) would be used in the compound interest formula. Now let's see these values in the formula:

A = P (1 + [r / n]) ^ (nt) A = 5,000 (1 + [0.05 / 12]) ^ (12 * 10) A = 5,000 (1.00417) ^ (120) A = 5,000 (1.64767) A = 8,238.35

In such a scenario, after ten years, you would have approximately 8,238 USD in your account. If we subtract the initial principal amount of 5,000 USD, you will have earned a net interest of 3,238 USD.